Background

Cost Adjustments are any discounts, chargebacks, rebates, and/or other price concessions given by the manufacturer or pharmacy to the Plan Sponsor that are attributable to Gross Retiree Costs between the Cost Threshold and Cost Limit. Cost Adjustments are not eligible for subsidy. Cost Adjustments need to be reported to CMS' RDS Center, as those amounts must be accounted for to determine the Allowable Retiree Cost.

Underestimating Cost Adjustments during interim payments occurs when a Plan Sponsor does not make changes to their Cost Adjustment methodology from one plan year to the next when the Cost Adjustment percentage has increased. During interim cost reporting, Plan Sponsors are required to report Estimated Cost Adjustments. The Estimated Cost Adjustment needs to be based on historical data and generally accepted actuarial principles. Plan Sponsors that do not update their estimating percentage based on historical data are at risk of reporting a lesser amount during the new plan year's interim payment requests, which will lead to an overpayment at Reconciliation.

Resources Related to This Issue

- Refer to Prepare Cost Data in the RDS User Guide for information on estimating Cost Adjustments.

- For information on allocating rebates and other price concessions, review CMS Retiree Drug Subsidy Guidance: Rebates and Other Price Concessions.

Examples

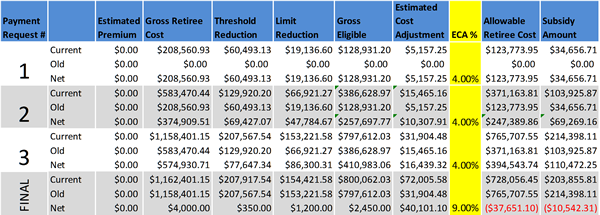

Example 6 depicts a Plan Sponsor whose system is set to estimate Cost Adjustments at 4% during interim payments. The Plan Sponsor does not make adjustments based on historical data. From 2007-2009, the Plan Sponsor's Actual Cost Adjustment was 8.75%. This example is for the 2010 plan year. The example displays the three interim payment requests and the final payment request.

The highlighted column provides the Estimated Cost Adjustment percentage. In the "Payment Request #1" rows, the Plan Sponsor is reporting a 4% Cost Adjustment. We arrive at the 4% by dividing the Estimated Cost Adjustment amount by the Gross Eligible. In this case, $5,157.25 / $128,931.20 = 0.04. For the second and third payment requests, the Plan Sponsor is reporting the same 4% Estimated Cost Adjustment. At Reconciliation, the Plan Sponsor's Cost Adjustment percentage has increased to 9% ($72,005.58 / $800,062.03).

Example 6: Cost Adjustment Percentage Underestimated for 2010 Application

The increase in the Cost Adjustment percentage caused the total Subsidy paid to be reduced. Total Subsidy paid during interim payments for the 2010 plan year is as follows: $34,656.71 + $69,269.16 + $110,472.25 = $214,398.11. Final Subsidy for this application is $203,855.81. The Plan Sponsor in Example 6 now has an overpayment in the amount of $10,542.31 ($214,398.11 - $203,855.81 = ($10,542.31)).

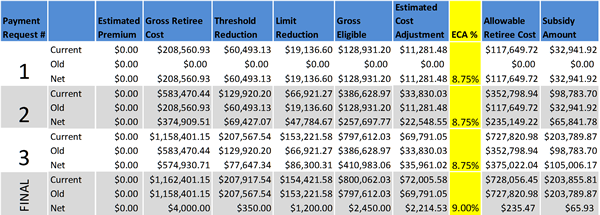

If the Plan Sponsor had used its historical data and adjusted its Estimated Cost Adjustment percentage during interim payments, it would not have been in an overpayment situation. Example 7 displays the Estimated Cost Adjustment percentage being changed from 4% to 8.75% during interim payments. The Estimated Cost Adjustment dollar amount was increased for each of the three interim payment requests when compared to the dollar amounts in Example 6. For Payment Request #1, Example 6 displays $5,157.25 in Cost Adjustments compared to $11,281.48 in Example 7. The same holds true for Payment Requests #2 and #3.

Example 7: Cost Adjustment Percentage Properly Estimated for 2010 Application

Due to the increase in Cost Adjustment percentage, the total Subsidy paid during the three interim payment requests decreased. Total Subsidy paid during interim payments for the 2010 plan year is as follows: $32,941.92 + $65,841.78 + $105,006.17 = $203,789.87. Final Subsidy for this application is $203,855.81. The Plan Sponsor is in an underpayment situation ($203,855.81 - $203,789.87 = $65.93), and is owed money by CMS' RDS Center.